Головна сторінка Випадкова сторінка

КАТЕГОРІЇ:

АвтомобіліБіологіяБудівництвоВідпочинок і туризмГеографіяДім і садЕкологіяЕкономікаЕлектронікаІноземні мовиІнформатикаІншеІсторіяКультураЛітератураМатематикаМедицинаМеталлургіяМеханікаОсвітаОхорона праціПедагогікаПолітикаПравоПсихологіяРелігіяСоціологіяСпортФізикаФілософіяФінансиХімія

Виховання вольової поведінки

Дата добавления: 2015-09-15; просмотров: 573

|

|

We begin with an inherently discrete-time system most of us are familiar with, namely, a fixed interest loan with constant periodic payments. An amount of money is borrowed for a specified period of time, and equally spaced instalments are paid to the lender until the loan is completely repaid. The interest rate on the loan is established at the time of the loan. Furthermore, each payment consists of a portion that reduces the loan principal and the remaining portion that is interest on the outstanding balance.

The situation is illustrated in Figure 3.1.

Fig. 3.1 Repayment and amortization of a loan.

The system parameters consist of:

: Loan amount

: Loan amount

: Interest rate per period (fixed for the duration of the loan)

: Interest rate per period (fixed for the duration of the loan)

: Number of interest periods for duration of loan

: Number of interest periods for duration of loan

The discrete-time input

| (3.3) |

is the constant payment A made at the end of the  th interest period. The discrete-time outputs are

th interest period. The discrete-time outputs are

: Outstanding balance of loan immediately following the th payment

: Outstanding balance of loan immediately following the th payment

: Portion of th payment used to reduce the outstanding balance

: Portion of th payment used to reduce the outstanding balance

: Interest portion of th payment

: Interest portion of th payment

The unpaid balance after the  st payment is simply the unpaid balance following the th payment plus the interest accrued for one period on the unpaid balance minus the amount of the st payment. Thus,

st payment is simply the unpaid balance following the th payment plus the interest accrued for one period on the unpaid balance minus the amount of the st payment. Thus,

| (3.4) |

| (3.5) |

, the portion of

, the portion of  used for loan principal reduction, is equal to the reduction in outstanding balance from the th to the st payment, that is,

used for loan principal reduction, is equal to the reduction in outstanding balance from the th to the st payment, that is,

| (3.6) |

, the interest portion of  , is obtained from

, is obtained from

| (3.7) (3.8) |

It can be shown that the constant payment  necessary to fully repay the loan in periods, that is, make

necessary to fully repay the loan in periods, that is, make  , is given by

, is given by

| (3.9) |

Equations (3.5), (3.6), and (3.8) are the difference equations for the first-order discrete-time system in Figure 3.1.

Task

A car loan in the amount of $125,000 is to be paid off in 30 years with an annual interest rate of 8%. Use the Simulink loan simulation to find

(a) The monthly instalment

(b) The unpaid balance after the 120th payment

(c) The principal portion of the 200th payment

(d) The total interest paid over the life of the loan

(e) The time required for the unpaid balance to equal $62,500

Note the use of a single ‘‘Unit Delay’’ block to generate the signal and the sum block in the upper right corner producing  as the difference of

as the difference of  and the payment amount according to Equation (3.5).

and the payment amount according to Equation (3.5).

Use Backward (implicit) Euler ‘‘Discrete–Time Integrator’’ for accurate computing.

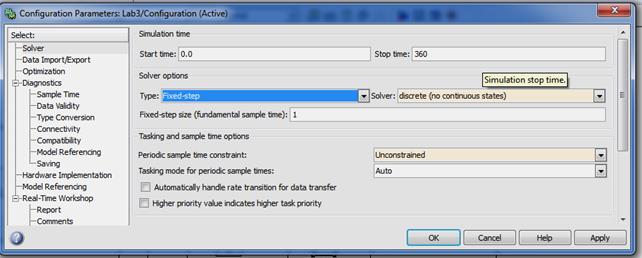

The ‘‘Simulation Parameters’’ dialog box is shown in Figure 3.2. A ‘‘Fixed–step’’ integrator with ‘‘Fixed-step size’’ of 1 is selected to force the simulation to step through integer values of discrete time. Since there is no continuous-time integration present in an inherently discrete-time system, the ‘‘discrete (no continuous states)’’ option is chosen from the drop-down menu of integrators.

Fig. 3.2 Simulation parameters dialog box for loan simulation.

The unpaid balance is shown in Figure 3.3. As expected, the loan balance is zero following the 360th monthly payment.

Fig. 3.3 Unpaid balance vs. interest period .

The total monthly payment , interest portion , and principal portion are shown in Figure 3.4. Note that the early payments consist almost entirely of interest with only a small amount going towards principal reduction. As the loan progresses, the portion of each monthly instalment used to reduce the outstanding balance increases. Conversely, the interest portion of each subsequent payment is less than the previous one.

The total interest paid over the life of the loan is computed in two different ways. The simplest approach is to compute  .

.

Fig. 3.4 Monthly installment , interest portion , and principal portion vs.

A Simulink diagram of the system is shown in Figure 3.5.

Fig. 3.5 Simulink diagram of loan repayment

Vocabulary:

| loan | кредит |

| loan amount | сумма кредита |

| loan repayment | погашение кредита |

| interest rate | процентная ставка |

| total interest paid | суммарные выплаченные проценты |

| installment | очередной взнос |

| interest portion | выплаченные проценты по кредиту |

| principal portion | погашение тела кредита |

| <== предыдущая лекция | | | следующая лекция ==> |

| Невербальні засоби спілкування | | | ФАРМАКОТЕРАПІЯ ЗАХВОРЮВАНЬ СЕРЦЕВО-СУДИННОЇ СИСТЕМИ. |