И.Р.)Dividend Discount Model

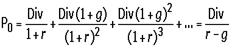

Dividend discount model (DDM) - a procedure for valuing the price of a stock by using predicted dividends and discounting them back to present value. The idea is that if the value obtained from the DDM is higher than what the shares are currently trading at, then the stock is undervalued. According to the DDM, dividends are the cash flows that are returned to the shareholder. The model requires loads of assumptions about companies' dividend payments and growth patterns, as well as future interest rates. The Dividend Discount Model is a way of valuing a company based on the theory that a stock is worth the discounted sum of all of its future dividend payments. In other words, it is used to evaluate stocks based on the net present value of the future dividends. To value a company using the DDM, you calculate the value of dividend payments that you think a stock will throw-off in the years ahead. Here is what the model says:

Where: P= the price at time 0, r= discount rate For simplicity's sake, consider a company with a $1 annual dividend. If you figure the company will pay that dividend indefinitely, you must ask yourself what you are willing to pay for that company. Assume expected return, or, more appropriately in academic parlance, the 'required rate of return' is 5%. According to the dividend discount model, the company should be worth $20.00 ($1.00 /.05). How do we get to the formula above? It's actually just an application of the formula for a perpetuity:

The obvious shortcoming of the model above is that you'd expect most companies to grow over time. If you think this is the case, then the denominator equals the expected return less the dividend growth rate. This is known as the constant growth DDM or the Gordon Model after its creator, Myron Gordon. Let's say you think the company's dividend will grow by 3% annually. The company's value should then be $1.00 / (.05 -.03) = $50.00. Here is the formula for valuing a company with a constantly growing dividend, as well as the proof of the formula:

This procedure has many variations, and it doesn't work for companies that don't pay out dividends. The classic dividend discount model works best when valuing a mature company that pays a hefty portion of its earnings as dividends, such as a utility company. In truth, the dividend discount model requires an enormous amount of speculation in trying to forecast future dividends. Even when you apply it to steady, reliable, dividend-paying companies, you still need to make plenty of assumptions about their future. The first big assumption that the DDM makes is that dividends are steady, or grow at a constant rate indefinitely. Stock analysts build complex forecast models with many phases of differing growth to better reflect real prospects. But even for steady, reliable, utility-type stocks, it can be tricky to forecast exactly what the dividend payment will be next year, never mind a dozen years from now. Another sticking point with the DDM is that no one really knows for certain the appropriate expected rate of return to use. It's not always wise simply to use the long-term interest rate because the appropriateness of this can change.

|