Stability and the Parameter Space

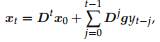

In Chap.3, we found (p. 36) that, for linear models of the form (10.1), we could write the state vector as

where D = F − gw′ is the discount matrix. So for initial conditions to have a negligible effect on future states, we need Dt to converge to zero. There- Definition 10.3. The model (10.1) is said to be stable if all eigenvalues of D = F − gw′ lie inside the unit circle. Stability is a desirable property of a time series model because we want models where the distant past has a negligible effect on the present state.

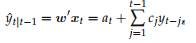

where at = w′ Dt−1x0 and cj = w′ Dj−1g. Thus, the forecast is a linear func- Definition 10.4. The model (10.1) is forecastable if

Obviously, any model that is stable is also forecastable.

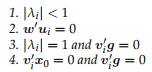

10.2 Stability and the Parameter Space 153 On the other hand, it is possible for a model to have a unit eigenvalue for D, but to satisfy the forecastability condition (10.3). In other words, an unstable model can still produce stable forecasts provided the eigenvalues which cause the instability have no effect on the forecasts. This arises because D may have unit eigenvalues where w′ is orthogonal to the eigenvectors corresponding to the unit eigenvalues. To avoid complications, we will assume that all the eigenvalues are dis-

where ui is a column of U (a right eigenvector) and vi is a row of V (a left eigenvector). By inspection, we see that the sequence converges to zero pro-

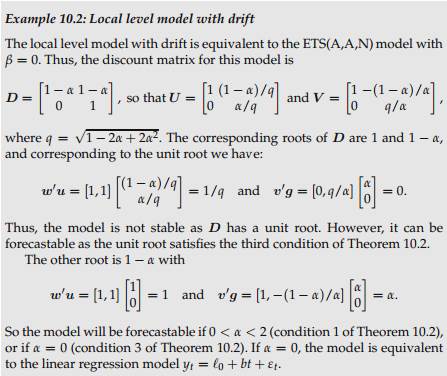

In this case, the sequence converges to a constant if and only if either |λi | ≤ Theorem 10.2. Let λi denote an eigenvalue of D = F − gw′, and let ui be the

The concept of forecastability was noted by Sweet (1985) and Lawton We now establish stability and forecastability conditions for each of the linear models. For the damped models, we assume that φ is a fixed damp-

154 10 Some Properties of Linear Models

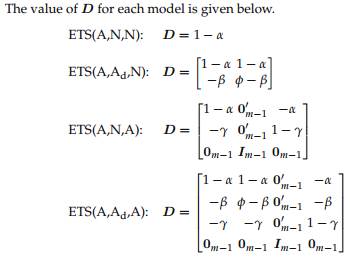

Again, for ETS(A,A,N) and ETS(A,A,A), the corresponding result is obtained from ETS(A,Ad,N) and ETS(A,Ad,A) by setting φ = 1.

The stability conditions for models without seasonality (i.e., ETS(A,N,N),

10.2 Stability and the Parameter Space 155

Fig. 10.1. Parameter spaces for model ETS(A,Ad,N). The right hand graph shows the

in McClain and Thomas (1973) for the ETS(A,A,N) model; results for the

|